You-tube

You-tube

Everything your finance team needs to close books accurately, on time, and without the last-minute chaos from a step-by-step checklist to best practices that actually work.

What is the Month-End Close Process?

The month-end close process is a structured accounting routine carried out at the end of every month to ensure financial records are accurate, complete, and ready for reporting. It involves reconciling accounts, reviewing transactions, posting adjusting journal entries, and preparing financial statements.

In practice, it means reviewing the company’s balance sheet, intercompany trades, month-end journal entries, and supporting documents such as bank statements and expense records then reconciling all of it so the books reflect reality.

For public companies, this is a mandatory fiscal reporting requirement. For private businesses, it’s simply good financial hygiene one that enables smarter decisions, smoother year-end processes, and stronger control over cash flow.

“Businesses that wait until year-end to prepare financial reports often find the task overwhelming. Monthly closes turn an annual ordeal into a manageable, ongoing rhythm.”

Why the Month-End Close Process Matters

At its core, the month-end close gives your business an accurate, timely picture of its financial position. Rather than operating on stale data, your team can track key performance indicators month-over-month, catch anomalies early, and make strategic decisions based on real numbers.

It also makes year-end significantly less painful. When books are properly closed each month, the annual process becomes a matter of summarising what’s already been verified not scrambling to reconstruct a year’s worth of transactions.

Increasingly, finance teams are adopting AI-driven and automated approaches to monthly closing, which reduces manual effort, minimises errors, and enables a faster, more reliable close cycle.

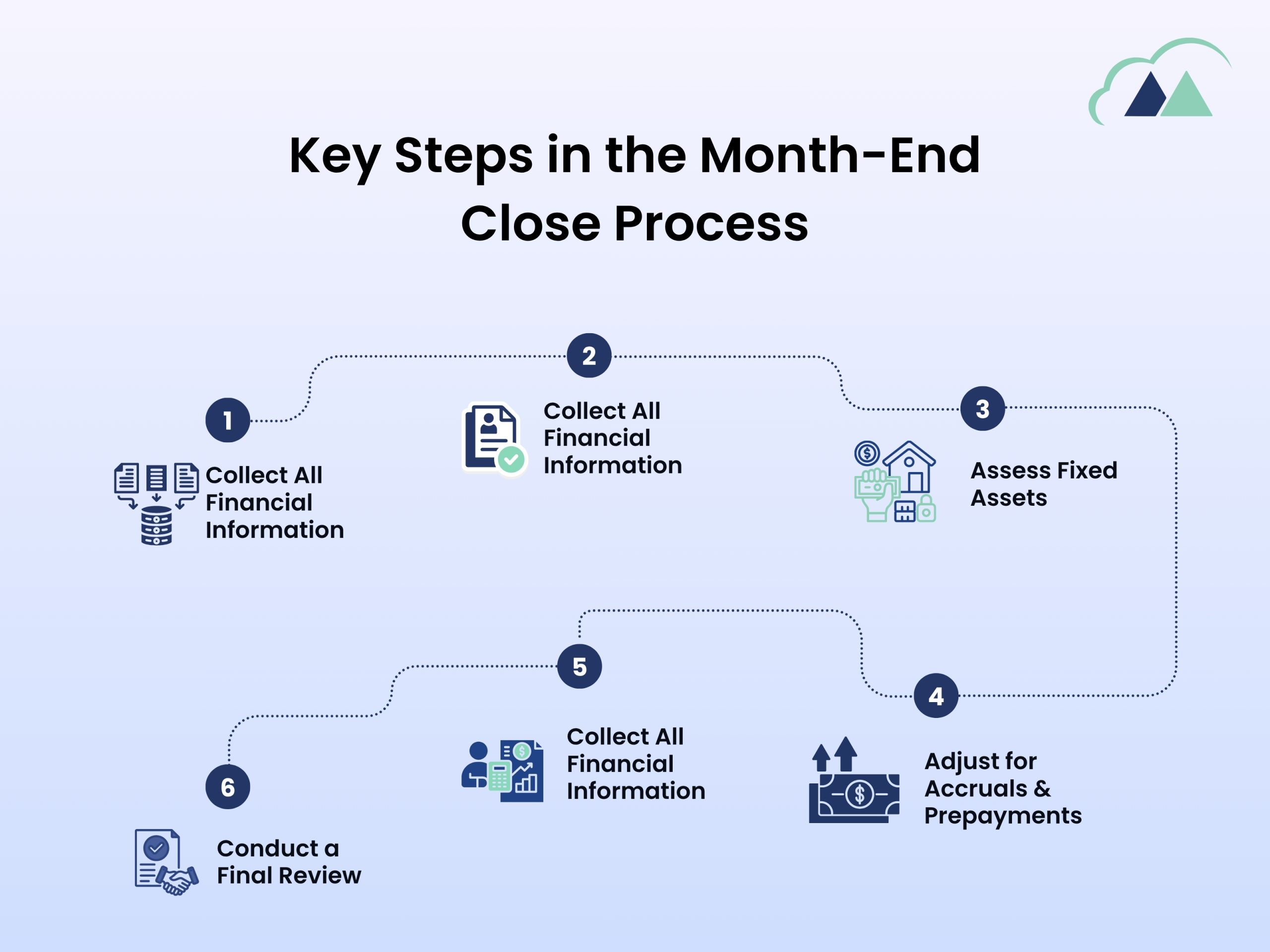

6 Key Steps in the Month-End Close Process

Most businesses follow these six steps to close their books each month. While the specifics will vary by company size and structure, the sequence is broadly consistent.

1. Collect All Financial Information

Gather all relevant data: accounts receivable, accounts payable, expense records, payroll, and any other transactions that occurred during the month. This is the raw material for everything that follows.

2. Verify and Reconcile the Data

Cross-check all transactions against receipts, bank statements, and other source documents. Every balance sheet account — cash, savings, checking — must be reconciled to establish a clear picture of cash flow.

3. Assess Fixed Assets

Review all fixed assets such as equipment, technology, vehicles, and property. Account for depreciation and ensure the depreciation expense is correctly categorised in the books.

4. Adjust for Accruals & Prepayments

Record accrued expenses (incurred but not yet paid) and allocate prepaid costs to the correct accounting period. These adjustments ensure the income statement accurately reflects the month’s activity.

5. Prepare Financial Statements

Compile the balance sheet, income statement, and cash flow statement. Verify that entries are correct and that there are no discrepancies between statements before moving to the final review.

6. Conduct a Final Review

Have senior management or an independent reviewer examine the statements with fresh eyes. This catch-all step ensures the financial close process reports are error-free before being finalised and distributed.

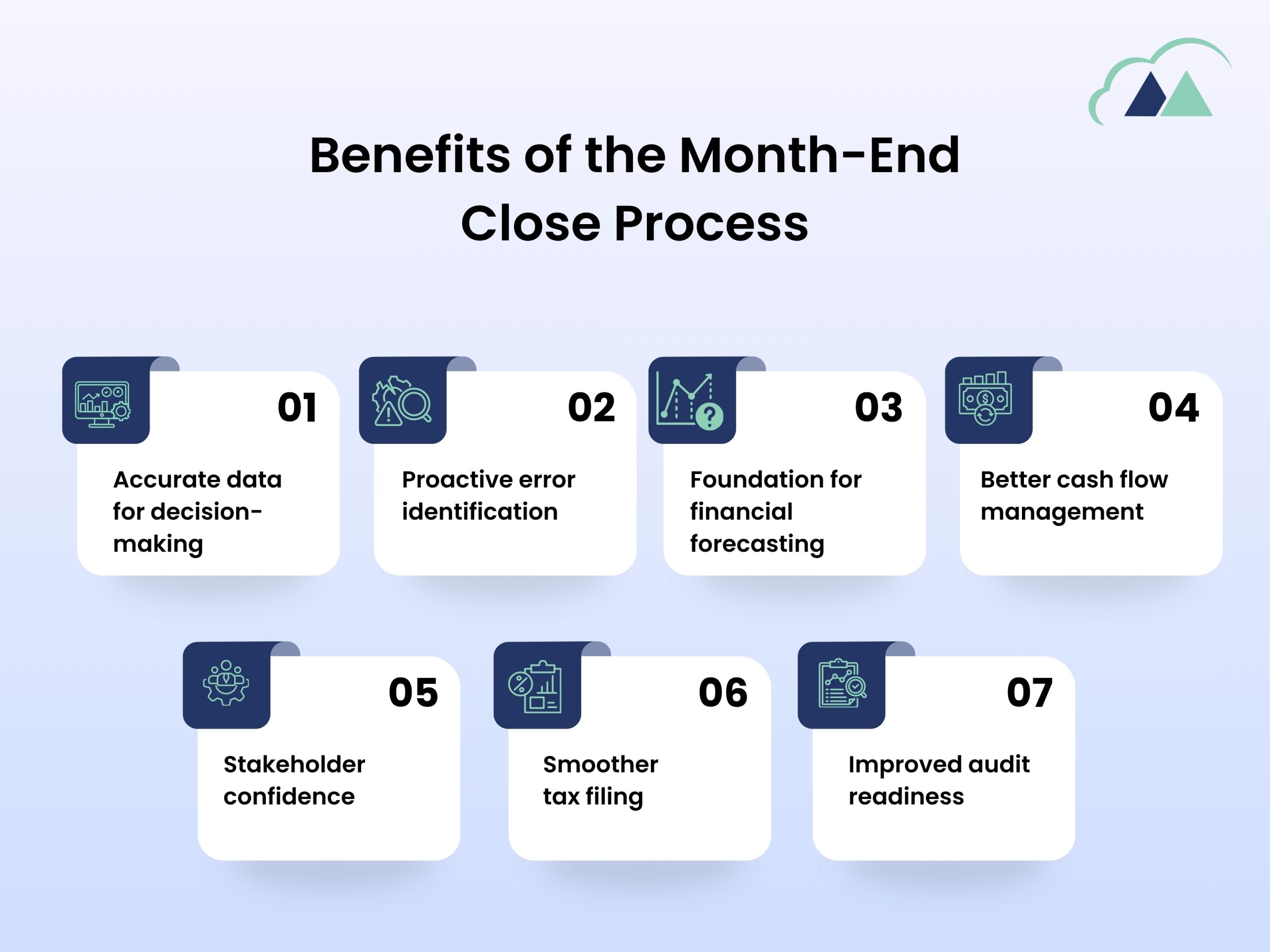

Benefits of the Month-End Close Process

A well-executed month-end close isn’t just an administrative exercise it delivers real business value. Here’s what your organisation stands to gain.

1. Accurate data for decision-making

Precise, up-to-date financials give leadership the confidence to make strategic calls from hiring and investment to cost control and pricing.

2. Proactive error identification

Catching discrepancies monthly rather than annually means problems are smaller, easier to diagnose, and far less costly to fix.

3. Foundation for financial forecasting

Reliable monthly records make budgeting and forecasting dramatically more accurate, enabling realistic goal-setting and efficient resource allocation.

4. Better cash flow management

Proper financial closure helps track liquidity in real time, ensuring the business can meet obligations and seize opportunities as they arise.

5. Stakeholder Confidence

Accurate, timely reporting builds trust with investors, lenders, and board members supporting stronger relationships and better access to capital.

6. Smoother tax filing

Organised monthly records eliminate the year-end scramble, making tax compliance straightforward and reducing the risk of penalties.

7. Improved audit readiness

When every month is properly documented and reconciled, audits become far less stressfull your team can respond to requests quickly and confidently.

Common Challenges with the Month-End Close

Despite its importance, the month-end close is often one of the most stressful periods in the finance calendar. Understanding the most common pain points is the first step to addressing them.

Fragmented data systems

Multiple ERPs, spreadsheets, and disconnected tools create data silos that slow consolidation and introduce errors.

Manual, error-prone processes

Heavy reliance on spreadsheets and manual journal entries adds time, inconsistency, and pressure to the close cycle.

Tight deadlines and burnout

Most organisations aim for a 5–10 day close, yet many exceed this — leading to rushed work and team burnout.

Poor visibility and communication

Without real-time tracking and clear role ownership, bottlenecks go undetected until the last minute.

Legacy systems

Outdated tools can’t handle multi-entity, multi-currency, or evolving regulatory requirements forcing manual workarounds.

No standardisation or controls

Without documented procedures and review workflows, inconsistencies multiply from one month to the next.

Late-arriving data

Critical accrual data and financial entries often arrive after the close has started, pushing teams into crisis mode.

Complexity from scale

Multi-entity consolidations and evolving compliance requirements make accuracy harder as the business grows.

Best Practices for a Faster, Cleaner Close

Improving your month-end close doesn’t require a complete overhaul. These six practices will have a meaningful impact regardless of your current maturity level.

1. Prioritise quality over speed

Rushing through the close and introducing errors compounds problems — especially when these statements feed into year-end reporting. Accurate records improve transparency and make KPI tracking meaningful.

2. Standardise with checklists and templates

A consistent approach ensures nothing is missed and makes onboarding new team members far easier. Templates also create an audit trail of who did what and when.

3. Review regularly and improve continuously

Note every roadblock you encounter during each close. If data collection is the bottleneck, invest in better data organisation mid-month. Treat each close as an opportunity to improve the next one.

4. Commit to and protect deadlines

Consistent reporting timelines help teams plan their work effectively. If current timelines are genuinely unrealistic, surface this early and work toward a phased improvement plan rather than accepting perpetual delays.

5. Automate wherever possible

From data collection to account reconciliation, automation dramatically reduces the time and effort involved in the close. It also reduces errors and makes it easier to share statements across teams.

6. Communicate clearly and in real time

When accounting teams share updates transparently, bottlenecks get addressed early. Clear ownership of each task — with real-time visibility — prevents the last-minute surprises that derail timely closes.

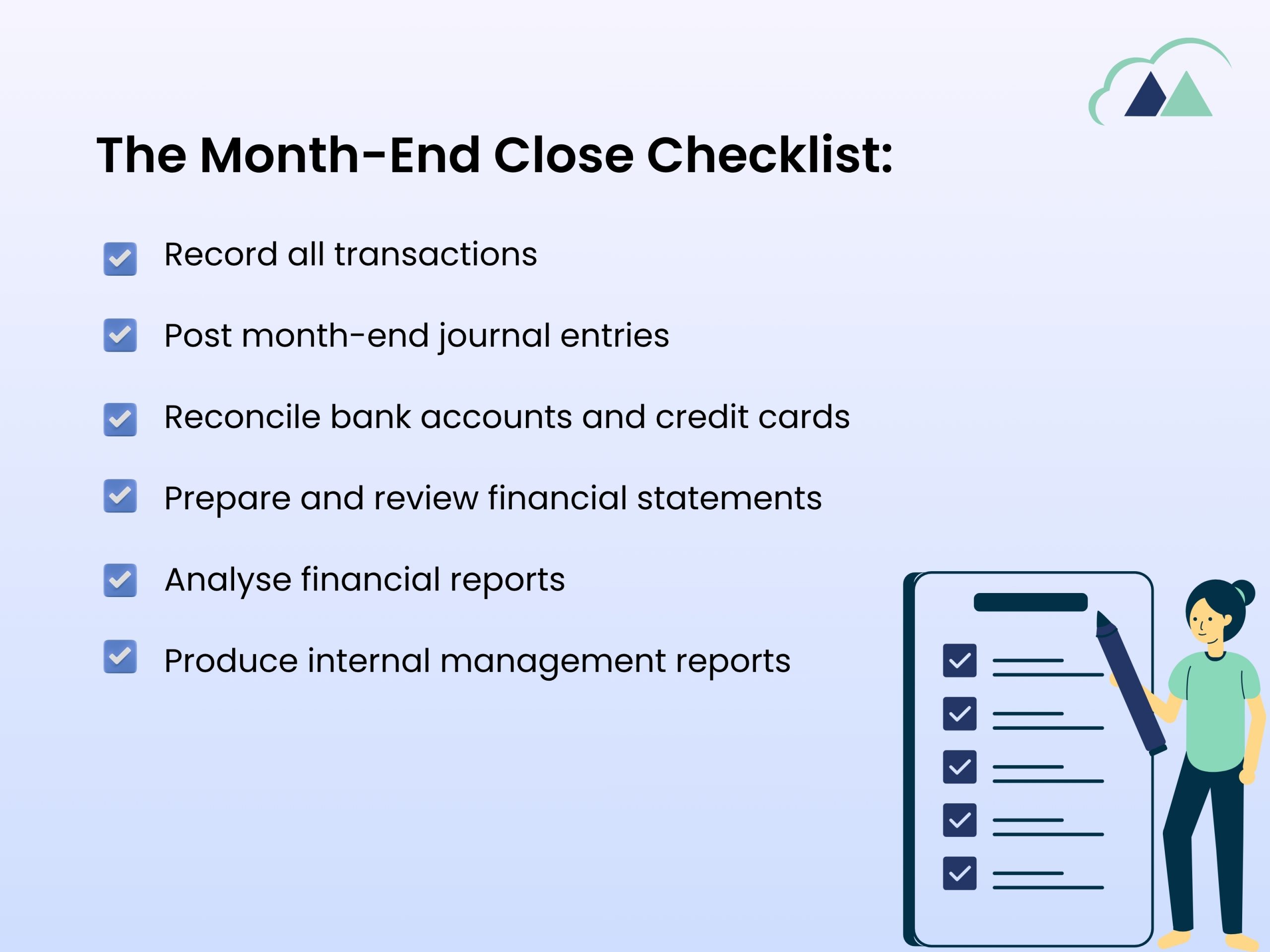

The Month-End Close Checklist

A structured checklist is one of the simplest and most effective — ways to bring consistency and accountability to your close process. Tasks should follow the same sequence in which they’re actually carried out; for example, recording bank transactions should appear before reconciling them.

✓ Record all transactions

Ensure all activity across bank accounts, accounts receivable, accounts payable, and credit cards is accurately captured. This is the foundation of everything that follows.

✓ Post month-end journal entries

Record all necessary adjustments: prepaid expenses, accrued expenses, accrued payroll, depreciation, and any other period-end entries.

✓ Reconcile bank accounts and credit cards

Compare all transactions against their respective statements. Identify and resolve any discrepancies before moving forward.

✓ Prepare and review financial statements

Maintain and reconcile workpapers supporting key accounts, ensuring all balances align across the balance sheet, income statement, and cash flow statement.

✓ Analyse financial reports

Review the balance sheet, profit and loss, cash flow, general ledger, and sales summaries to verify completeness, accuracy, and consistency with prior periods.

✓ Produce internal management reports

Finalise reporting documents for leadership review giving decision-makers a clear, accurate picture of monthly financial performance.

Pro tip: Beyond reducing errors, a checklist enables continuous improvement. When close processes are documented, your team can identify exactly where delays occur and systematically address them over time.

Simplify Your Month-End Close Process

Eliminate manual reconciliation, reduce errors, and close your books faster with Madhda’s ERP-driven solutions.

Transform your financial operations with automation and real-time insights.

📞 Call: +1 (302) 303-9860

📧 sales@madhda.com